Packaging sector - Finding the right asset (Part 2/2)

West Pharmaceutical is the best asset to invest in the packaging sector.

Disclaimer: I am not a Registered Investment Advisor. The views and analysis expressed in this post are for educational and informational purposes only and do not constitute financial advice, investment advice, or a recommendation to buy or sell any securities.

This is part 2 of the 2-part series on packaging sector.

In the first part, I did a deep dive on the sector and its segments and identify which segment is(are) attractive from investment perspective.

Just a recap on why I wanted to explore packaging sector - there are 3 reasons:

It’s the pick and shovel for the consumption story of any country or category and is more predictable than consumer brands for example (read “consumer preferences are always shifting”). Thus, a safer and better way to play consumption growth story.

On the surface the sector seems fragmented with not attractive return metrics, thus not attracting attention of many investors and hence giving individual investors the opportunities to find mispriced assets if one digs deeper. There are pockets of growth, businesses with strong moats, and assets with higher return metrics. We’ll look into these aspects in the current and next part. This part will cover more from sector and segment attractiveness. The next part will cover more about companies operating in the most promised segments.

Finally, it’s an active sector among private equity investors, thus giving me the confidence that there’ll be buyers for these businesses if I pick attractive ones. After all, active investors’ participation is necessary for fair price discovery.

Below is the summary from part 1:

The packaging sector has 5 segments - metal, glass, corrugated & paper, plastic, and specialty packaging

Of the 5 segments, glass is the smallest at $60 B. Using this as base, corrugated & paper is the largest at 7x and plastic at 6x. Metal and specialty are among smallest at 2.5x each.

Growth - The segments can be bucketed into 2 types:

Type1: Specialty & pharma segment AND corrugated and paperboard - Specialty & Pharma were the fastest growing at 7% revenue growth and corrugated and paperboard growing close to 6%.

Type2: Remaining (Plastic, metal, and consumer glass) - These grew at <5% CAGR during the same period. More importantly, in the last 5 years, growth has slowed down further for type 2 to 2-3% growth

Market concentration - Consumer glass, metal, and specialty & pharma are more consolidated than others

Capex and switching cost

Glass and metal segments have higher capex intensity than other segments. maintenance capex is high for glass

Aluminum cans within metal packaging are capex intensive because of the extreme speed and precision of can-forming machinery

Plastic is the lowest “entry-level” segment

Pharma related packaging also requires upfront capex (depending its glass, plastic, elastomers, etc.) due to requirement of clean-room facilities, precision injection molding tooling, and assembly robotics.

In terms of switching cost, it’s the lowest in corrugated boxes and plastics segments, followed by consumer glass and metal, and the highest in pharma segment

RoCE -

Commoditized glass, Plastic, and metal segments have lower RoCEs ~ 10%.

Specialized glass, corrugated & paperboard, and pharma have higher RoCEs ~ 15%+

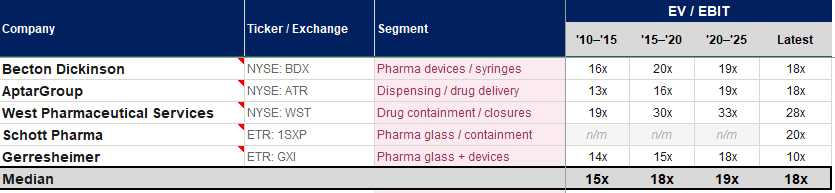

Valuation - Latest EV/EBIT is around 18x for pharma vs 12x for other segments except consumer glass which trades at much lower at 8x

Conclusion - In my opinion, pharma packaging segment is the most attractive segment from investment perspective. Sector drivers are not cyclical with switching costs being high due to FDA files lock-in. The end-use market, which is biologics, is growing at >10% CAGR. The segment growth currently is supported by tailwind of GLP-1, ageing populations, and biosimilars and has large headroom to grow. Moreover, the best asset can earn 15–20%+ ROCE consistently over long term. All these positive traits come with a risk - substitution risk from cyclic olefin polymer (COP) plastic.

In this part, I’ll focus on key global players, their position and competitive advantage, product differentiation, and which companies within pharma segment is attractive from asset quality and investment perspective.

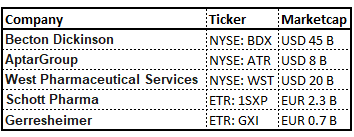

In my research, I found these 5 scaled companies in pharma packaging segment -

Becton Dickinson

AptarGroup

West Pharmaceutical

Schott Pharma

Gerresheimer

Let’s dive deep into these companies from following perspectives:

Business/Product description

Business quality

Financial/operating metrics

Management quality

Capital allocation

Valuation

1. Becton Dickinson (BD)

1.1. About the business

BD is a leading global medical technology company, and one of the world’s largest suppliers of syringes, needles, and drug delivery systems. Its products include pre-filled syringes, insulin pens, infusion pumps, and surgical instruments

The market cap is USD 45 B and the company generated USD 21.8 B in revenue in FY25. BD is aggressively investing in GLP-1 drug delivery. In January 2026, BD announced a $110 million investment to expand prefillable syringe production at its Columbus, Nebraska facility, targeting mid-2026 supply start. The company aims to build GLP-1 drug delivery into a $1 billion product category by 2030. BD also ramped up U.S. syringe production in 2024 after the FDA warned against some Chinese syringes, demonstrating its ability to flex production to meet quality-driven constraints

The company has announced to separate biosciences and diagnostic solutions business to enhance focus and drive growth. Post the separation, there’ll be 4 segments:

Medical Essentials: The bedrock of the company, providing syringes, needles, and IV catheters. This segment leverages BD’s massive scale to maintain high market share in high-volume consumables.

Connected Care: This high-tech segment includes the Alaris infusion platform and the newly integrated Advanced Patient Monitoring (APM) unit (formerly Edwards Lifesciences’ Critical Care business).

Interventional: Focusing on specialty surgical products, oncology, and urology, this segment targets high-margin procedures and chronic disease management.

BioPharma Systems: A rapidly growing unit providing prefilled syringe systems, particularly for the surging GLP-1 and biologic drug markets

Medical essentials and BioPharma systems are the segments that overlap with the packaging sector.

1.2. Business quality

FDA lock in provides recurring revenue stream in BioPharma segment. Drug delivery devices such as injectors and prefilled syringes regulatory file lock in. Once a device is specified in drug’s approval, the device is locked in for the entire drug’s life.

Scale in Medical Essentials. BD produces over 34 billion medical devices annually, making it nearly impossible for smaller rivals to compete on price in medical essentials.

Higher switching cost for BD Alaris. BD's Alaris infusion system is one of the leading IV infusion pump platforms in hospital pharmacy settings. Hospitals standardize on BD syringes to avoid retraining. Switching to a competitor's system requires replacing hardware across the facility, rebuilding all drug protocols, retraining staff, and managing the transition risk. Switching

However, BD does not pass my quality test because the strict lock-in only applies to BioPharma segment which is just 8% of the total revenue. Also, the largest product category by volume that BD makes is syringes which is a commodity with no differentiation and this business has no moat.

2. Schott Pharma

2.1. About the business

Schott’s portfolio comprises drug containment solutions and delivery systems for injectable drugs ranging from prefillable glass and polymer syringes to cartridges, vials, and ampoules. From packaging sector perspective, it operates in glass primary packaging. The market cap is EUR 2.3 B and the company generated EUR 1 B in FY25. The sole owner of SCHOTT AG is the Carl Zeiss Foundation which has owned and led the scientific glass company for over a century. The company's Type I borosilicate glass formulation — the highest-specification pharmaceutical glass, used for biologics and injectables — is the product of long term materials science development.

2.2 Business quality

Premiumization story - Systematic shift away from standard glass vials toward High-Value Solutions (HVS) — ready-to-use, pre-washed, sterility-assured, and in some cases coated vials and syringes that require dramatically less processing at the pharmaceutical fill-and-finish site. This shifts processing cost from the pharma customer to SCHOTT, but at a price premium that is well in excess of SCHOTT's incremental cost.

Regulatory lock in - The HVS qualification has a deeper regulatory lock in than the standard vial specification

Schott does not pass the quality test because 43% of company’s revenue still comes from standard glass vial, which is a commodity.

3. Gerresheimer

3.1. About the business

Gerresheimer AG is a German manufacturer of primary packaging products for medication and drug delivery devices made of special-purpose glass and plastics. The products include insulin pens, autoinjectors, inhalers, micropumps, and digital therapy support systems.

The market cap is EUR 0.7 B and the company generated EUR 2.2 B during TTM (Aug 2025).

I did not dive further into it because I discovered various on-going issues related to governance and management change:

BaFin has expanded its investigation into Gerresheimer’s financial reporting for 2024 and 2025.

Former CFO Bernd Metzner and former CEO Dietmar Siemssen both stepped down amid the crisis, following pressure from activist investor Active Ownership Capital

The company has been criticized for over-relying on "one-off" adjustments to calculate adjusted EBITDA

The acquisition of Bormioli Pharma for €800 million was described by critics as a "diligence failure". The former CEO had close ties to the seller (Triton Partners), and Bormioli was reported to be experiencing severe financial losses and channel-stuffing at the time of purchase

Thus Gerresheimer does not pass the quality test.

4. Aptar Group

4.1. About the business

Aptar group is a global leader in drug delivery and consumer product dispensing, including dosing and protection technologies. The group has 3 segments: Aptar Pharma, Aptar Beauty, and Aptar Closures.

Aptar Pharma provides drug delivery systems, components and services globally. Products include: nasal spray pumps, MDI valves, dose indicators & counters, DPIs, electronic / connected devices, eye-droppers, vial stoppers, prefilled syringe (PFS) plungers.

Aptar Beauty creates added-value beauty packaging & dispensing solutions in fragrance, color cosmetics, skincare, and personal care - e.g. mist sprays, airless packaging, aerosol valves and bag-on-valve, lipstick packaging.

Aptar Closures offers dispensing closures such as BAP (Bonded Aluminum to Plastic), tethered caps, precision dispensing valves.

4.2. Business quality

Pharma is the largest segment contributing to two-third of its operating profit. Pharma segment’s growth is driven by strong demand for elastomeric components and nasal drug delivery technologies. The Pharma segment earns around 35% EBITDA margins.

Pharma segment offers recurring revenue due to FDA files lock in similar to Biopharma segment for Becton Dickinson or HVS segment for Schott Pharma.

Beauty and Closures are lower quality, more commoditised, and drag on overall performance.

Given that almost half of revenue and significant (one-third) operating profit comes from commoditized businesses, Aptar also does not pass the quality test.

5. West Pharmaceutical

5.1. About the business

West commands an estimated ~70% share of the global elastomeric components market for injectable drug packaging. Its nearest competitors (e.g. Swiss firm Datwyler, and Aptar Group) remain distant seconds, as West’s century of expertise, high-quality reputation, and regulatory embeddedness create strong barriers to entry. Below is the example of product types that it sells.

5.2. Business quality

Strong Moat: 100% of revenue comes from pharma packaging Pharmaceutical clients are extremely hesitant to switch packaging suppliers due to strict regulations and the costly re-validation process (the Drug Master File lock-in) required for even “commodity” components. This gives West a sticky customer base and pricing power for its critical yet low-cost healthcare components.

Growth drivers: The proliferation of biologic drugs, vaccines, and injectable therapies (e.g. the booming GLP-1 obesity/diabetes treatments) underpins steady long-term demand for West’s products. GLP-1 elastomer products accounted for 8% of total company revenues. West is even the world’s largest manufacturer of insulin auto-injectors, positioning it to benefit from surging use of injectable biologics. Additionally, pharma companies increasingly outsource high-value processes (like sterile packaging and self-injection devices) to West, expanding West’s value-add per unit.

5.3. Financial/operating metrics

Topline has grown at 8% CAGR during the last 10 years

Operating income has grown at 17% CAGR during the last 10 years

Net income has grown at 20% CAGR during the last 10 years

RoCE has increased over the years with last 5, 10, and 15 years average at 19%,18%, and 13% respectively. This is much higher than peers which averages around 13%

Last 5 and 10 years average operating cash flow margin was 20% and 19%, respectively, which are higher than the peers (16% and 17%, respectively for those 2 periods)

5.4. Management quality

The quality of good managers are those who:

Have meaningful networth tied to the business to have enough skin in the game

Allocates capital rationally to focus on long term shareholder returns

Is transparent about company’s performance, not just during good times but bad times too

Build durable competitive advantages

Let’s see how West Pharma scores against these:

Skin in the game: The current CEO (Eric Green) owns $46M worth of stock (0.23% of the company). In absolute terms the amount is high but not significant from holding % perspective. However, 0.2% ownership for CEO is at par with other US large caps.

Capital allocation: We will look into this in detail in the next section

Communication: Management was transparent in communicating the headwinds coming from covid-led destocking cycle. Despite the short-term guidance revisions, leadership maintained transparency regarding their long-term growth strategy, including investments in capacity expansions for GLP-1 and other biologics. I would have liked to have seen more conservative guidance from the management. The guidance released in Q42023 for 2024 full year was optimistic, ofcourse in hindsight. But guiding around 3% organic sales growth for 2024 and achieving -1.5% in actual performance is quite off. Moreover, after facing significant pressure in Q12024, with flat organic sales growth, management reaffirmed the full year guidance. Also, at the time of publishing 2023 full year result, the management had the view for first half of Q12024 and still didn’t adjust commentary meaningfully. Q12024 organic sales declined 3%. At this point, the CEO mentioned “We had a solid start to the year and our full-year 2024 financial outlook remains unchanged”. And guess what was the organic sales growth in Q22024? Negative 6%! At this point the management guided for lower sales growth which it met in 2024. So, overall, management guidance can be more transparent and timely.

Continue building of competitive advantage: Under the tenure of current CEO, Eric Green (since April 2015), West Pharmaceutical maintained its industry leading market share and the gap from the second largest player. The business has been executing well on scaling High Value Product (HVP) business which now accounts for 48% of sales. HPV segment has around 20% HIGHER gross margin than rest of the business. Not all credit should accrue to the management because they also get the benefit of regulatory tailwind - EU GMP regulations which has mandated upgrades to HVP products.

During the current CEO tenure (since April 2015), West Pharmaceutical has delivered shareholder return of 16.5% CAGR vs 6.6% for S&P 500 Healthcare index and 11.8% for S&P 500 (note that these are price return).

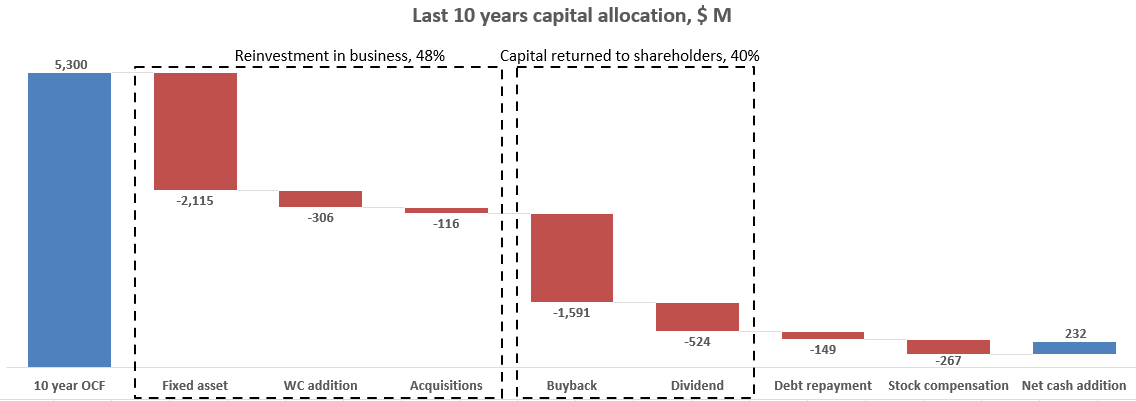

5.5. Capital allocation

Capital allocation is the most crucial aspect and this helps me to reject many investment opportunities (In investing business, we will eventually make decent money by just avoiding mistakes).

The way I evaluate capital allocation decision is very simple and as follows:

Take operating cashflows for the last 10 years and sum them up

Put them in various allocation buckets - dividend, buy back, fixed asset, acquisition, debt repayment, working capital, stock based compensation, and cash on books

I would like to see close to 50% or more to be returned to shareholders, depending on company’s growth phase and industry maturity

Below is how it looks for West Pharmaceutical:

As one can see, of $5.3 B operating cashflow that was generated in the last 10 years (2015-2025):

$2.5 B (48%) was redeployed in the business for growth.

$$2.1 B (40%) was returned to the shareholders with buyback being the mode of return

$261 M (5%) was used for SBC. Although, for accounting purposes, it’s a non-cash expense, I consider it as expense and dilutive to shareholders’ return. Hence, I don’t consider this cash available to be returned

This seems reasonable allocation as this is/will be a growth business for foreseeable future. And in such case returning ~40% of capital return to shareholders is a good number.

5.6. Valuation

I believe that West Pharmaceutical is the best asset to invest in the packaging sector among the scaled players. This is reflected in the premium valuation multiples that it gets. This is true for more than 15 years, as seen in the average EV/EBIT multiples for different 5 year periods. The current multiple is around 28x EV/EBIT. The current valuation is very much outside my comfort zone and I’m willing to wait. Moreover, further research is required to understand growth drivers, risks, and ongoing/upcoming CEO and CFO transition.

This concludes the 2 part series on the packaging sector.

I like this. Packaging is an underrated sector. For the right company, it can be a kind of non-cyclical hidden champion - and a perfect example of “picks and shovels.” Btw I even started thinking about how the actual picks and shovels were packaged, but that’s a side track...

The stocks you highlight are interesting. At the moment, I only own a small Indonesian pharmaceutical packaging company, but I could definitely see myself owning more companies of this kind in the future. Thanks for the great inspiration!